Tiếng Việt

Tiếng Việt 한국어

한국어 中文 (中国)

中文 (中国)Tax is one of the most important obligation of Company. According to current Vietnamese law, a Company has to pay various types of tax. In the article below, OTIS LAWYERS will share with readers the taxes that companies in VietNam must pay.

License fee

License fee is amount of money which has to be annually paid by Company. The amount of licensing fee is based on the charter capital written in the certificate of enterprise registration or investment capital written in the certificate of investment registration (for organization).

According to Clause 1, Article 4 of Circular No. 302/2016/TT-BTC, the amounts of licensing fees for organizations engaging in business as follows:

| Licensing fee level | Registered capital (Charter capital of investment capital) | Payment rate (VND/year) |

| – Level 1 | Greater than VND 10 billion | 3.000.000 |

| – Level 2 | Less than equal to VND 10 billion | 2.000.000 |

| – Level 3: Branches, representative offices, business premises, public service providers, other business entities. | 1.000.000 |

New organizations shall be exempted from license fees for the first year from the date of establishment (according to point c, clause 1, article 1 of Decree No. 22/2020/ND-CP). After exemption period, company shall pay license fees according to law regulation.

Deadline for declaring and paying the license fees:

* The declaration of license fees:

According to Clause 1, Article 5 of Decree No. 139/2016/ND-CP amended by Clause 3, Article 1 of Decree No. 22/2020/ND-CP, the declaration of license fees shall be made once when starting production/business or upon establishment. Company shall make and submit their declarations of license fee to their supervisory tax authorities by January 30 of the year following the year of commencement of production/business or the year of establishment.

* Payment of license fees

Deadline for paying license fees is every January 30 (according to point b, clause 1, Article 5 of Circular No. 302/2016/TT-BTC)

Corporate income tax

Corporate income tax (CIT) is one of the types of tax that FDI enterprises have to pay to the State.

CIT is a direct tax, levied on the taxable income of company including income from manufacturing activity, trading goods and services activity and other incomes as prescribed in regulations of law.

The corporate income tax period is determined according to the financial year and is calculated based on the business results shown in the annual financial statements. Previously, quarterly, based on the business situation as well as quarter declarations and reports submitted to the tax agency, the enterprise must temporarily pay CIT no later than the 30th day of quarter succeeding the quarter in which tax is incurred. Enterprises are not required to submit the provisional CIT declaration quarterly. (According to Article 17 of Circular No. 151/2014/TT-BTC).

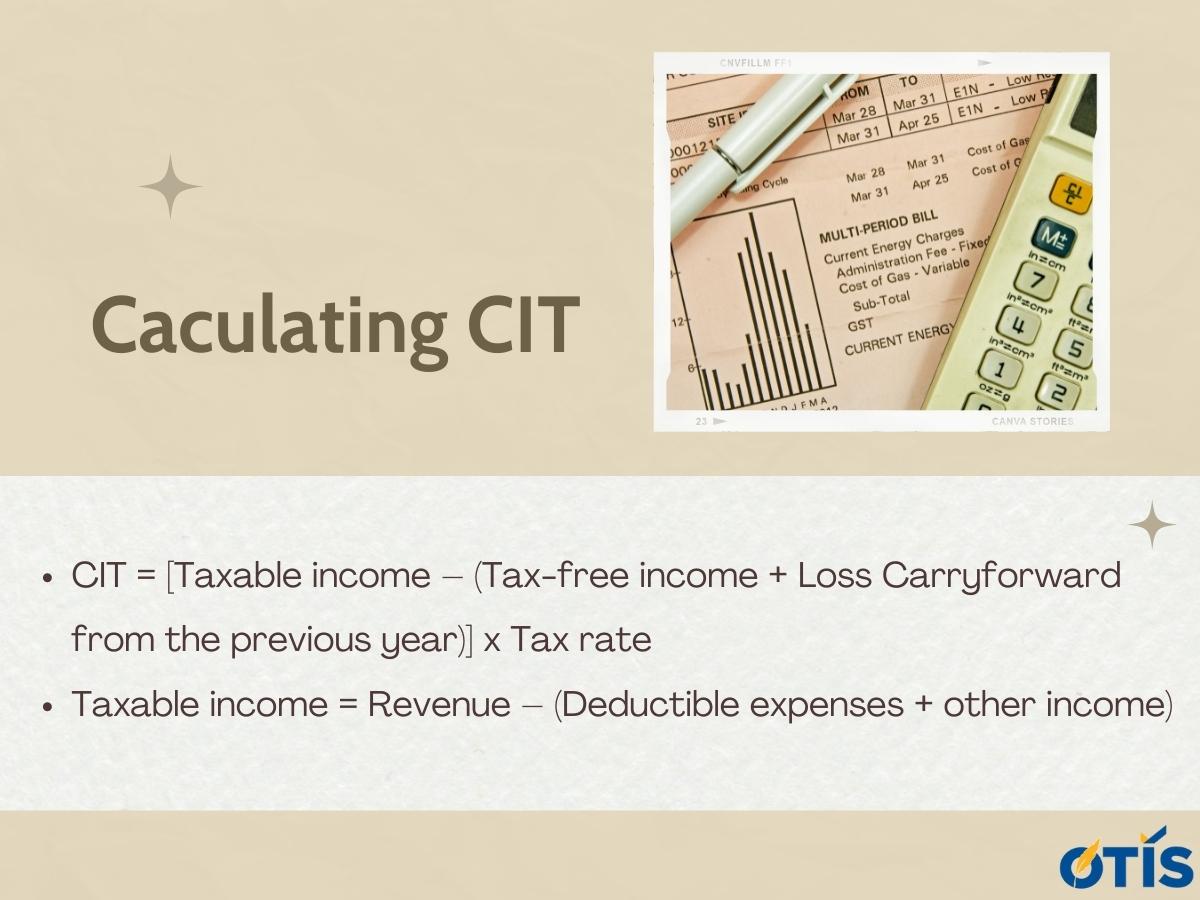

Caculating CIT

CIT rate: The current CIT rate is 20% applied to all enterprises (Article 11 of Circular No.78/2014/TT-BTC), excluding some enterprises applied preferential tax rates (Article 19 of Circular No.78/2014/TT-BTC) and some specific enterprises (searching, exploring, exploiting oil and rare resources)

Value Added Tax

Value Added Tax (VAT) is a tax calculated on the added value of goods and services arising in the process of manufacture, circulation and consumption in the territory of Vietnam.

Goods and services subject to VAT are those used for manufacture, trading, and consumption in Vietnam (including those purchased from overseas organizations and individuals), except for the goods and services in Article 4 of this Circular No. 219/2013/TT-BCT.

Payers of VAT are the organizations and individuals that manufacture, trade in taxable goods and services in Vietnam and the organizations and individuals that import goods or purchase services from abroad.

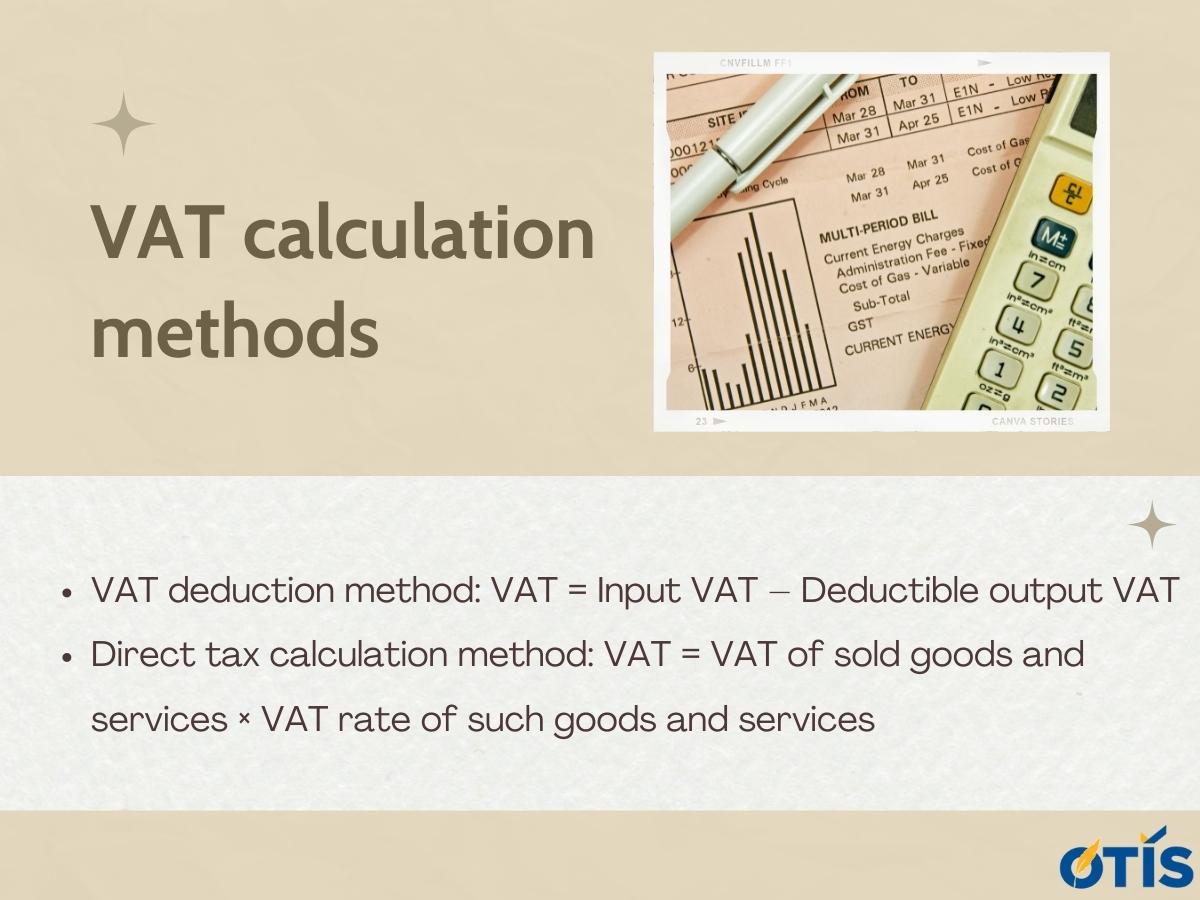

VAT calculation methods includes:

VAT declaration and payment period

Tax declaration period is divided according to each case: declaration by month, by quarter or by each time arising.

For business operations, most of companies apply the quarterly VAT declaration regime. This regime is applied to VAT payers whose total revenue from selling goods and providing services in the preceding year is VND 50 billion or less.

Deadlines for submitting tax declarations

According to Clause 3, Article 10 of Circular No.156/2013/TT-BTC, the deadlines for submitting tax declaration are:

- The deadline for submitting a monthly tax declaration is the 20th of the month succeeding the month in which tax is incurred.

- The deadline for submitting a quarterly tax declaration or provisional quarterly tax declaration is the 30th of the quarter succeeding the quarter in which tax is incurred.

- The annual tax declaration must be submitted by the 30th of the first month of the calendar year.

- The annual terminal declaration must be submitted within 90 days from the end of the calendar year or tax year.

Deadlines for paying tax

According to Clause 2, Article 26 of Circular No.156/2013/TT-BTC, deadline for paying tax is the deadline for submitting the tax declaration if tax is calculated by the taxpayer, or the deadline imposed by the tax authority or a competent authority.

Personal income tax

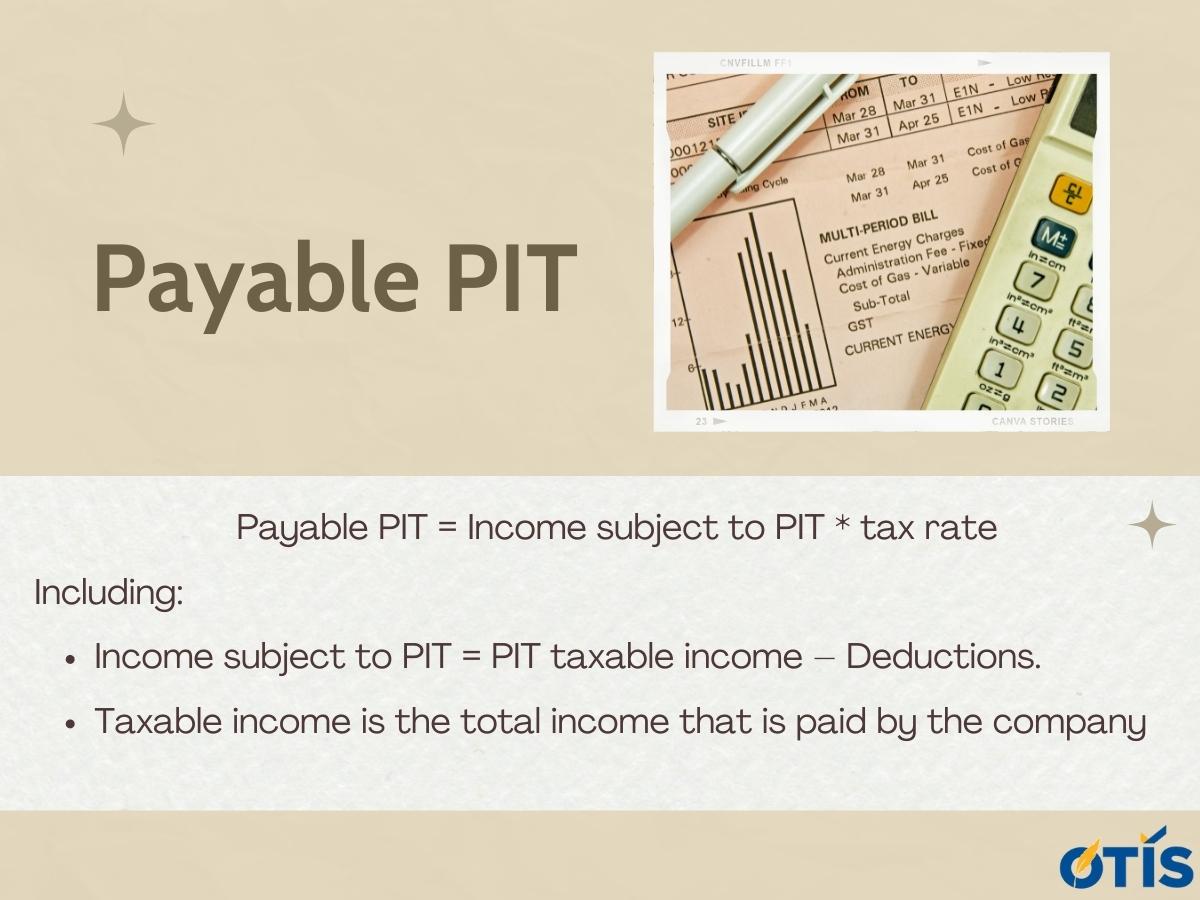

Personal income tax (PIT) is one of the taxes that businesses need to pay on behalf of employees calculated on a monthly basis. PIT is declared monthly or quarterly, but finalized annually.

The deductions include family deduction in which: deduction for taxpayer is 11,000,000 VND/person/month; deduction for each dependent is VND 4,400,000/person/month.

Some other taxes based on the operation field of enterprises

Resource tax is an indirect tax which is paid to the State by organizations and individuals when exploiting natural resources.

Import and export tax is an indirect tax, levied on goods exported or imported through Vietnam’s border; goods traded and exchanged by border residents and other goods considered as imported and exported goods.

Environmental protection tax is an indirect tax, levied on products and goods causing adverse impacts on the environment. Environment tax is applied to enterprises producing and importing taxable goods as prescribed in the Law on Environmental Protection Tax 2010.

Special consumption tax is an indirect tax, levied on a number of special goods directly produced and sold by enterprises or imported and sold by enterprises. Special consumption tax is applied to enterprises producing or importing taxable goods or services.

Non-agricultural land use tax is a direct tax levied on non-agricultural land used for production, implementation of investment projects, and construction of offices.

This is OTIS LAWYERS’s advice regarding taxes that FDI enterprises may have to pay when operating in Vietnam. When operating in Vietnam, if investors and companies have difficulties in the process of declaring and paying taxes, please contact us for being supported and provided with our accounting service. If you have any questions about taxes, please contact us by phone or email for advice.

OTIS LAWFIRM & PARTNERS

Address: K28 Lane 68 Trung Kinh, Yen Hoa Ward, Cau Giay District, Hanoi

Mobile: 0987.748.111

Email: info@otislawyers.vn

{kind=link}

{kind=link}

Comments