Tiếng Việt

Tiếng Việt 한국어

한국어 中文 (中国)

中文 (中国)

Import tax is a type of duty imposed by the state on goods produced in other countries and territories. So, what exactly is import tax? How is import tax calculated? Read OTIS LAWYERS‘ article below for detailed explanations.

Overview of Import Tax

What is Import Tax?

“Import tax is a type of indirect tax levied by a country/territory on goods imported from abroad.”

When goods are transported by means of transportation to the border gate, customs officials inspect the goods based on the declaration and calculate the import tax according to regulations. Import tax must be paid before clearance so that the importer can circulate the goods within the country. To calculate import tax, goods subject to tax are classified under the Harmonized Commodity Description and Coding System (established and continually developed by the World Customs Organization).

Purpose of Import Tax

The primary purpose of import tax is to increase revenue for the budget. Additionally, import tax aims to:

– Make imported goods more expensive compared to domestic substitutes, reducing trade deficits;

– Counteract dumping by increasing the price of dumped goods to the general market level;

– Counteract tariff barrier actions by other countries that impose taxes on Vietnamese exports, especially in trade wars;

– Protect important production sectors (such as agriculture);

– Safeguard new industries until they are strong enough to compete internationally;

– Provide a basis for trade negotiations when implementing trade preferences or retaliatory trade measures due to transparency and ease of implementation.

Regulations on Import Tax to be Aware of

Entities Subject to Import Tax

Based on Article 3 of the Law on Export and Import Duties 2016, entities subject to import tax include:

– Enterprises or organizations, individuals as owners of imported goods;

– Organizations entrusted with importing goods;

– Individuals importing goods upon entry or receiving goods at Vietnam’s border;

– Customs clearance agents authorized to pay taxes;

– Banks, credit institutions paying taxes on behalf as per regulations.

Import Tax Schedule

The import tax schedule is a comprehensive table of tax rates prescribed by the state for entities subject to import tax. It serves as a basis for identifying tariff rates for imported goods.

The import tax schedule includes the following types:

– Preferential import tax: A type of import tax for goods originating from countries with trade relations under the Most Favored Nation policy (MFN). This policy applies to approximately 180 countries worldwide.

– Special preferential import tax: A special type of import and export duty applied to goods imported from countries with bilateral/multilateral trade agreements with Vietnam, such as ACFTA, ATIGA, AJCEP, VJEPA, AKFTA, AANZFTA, AIFTA, VKFTA, VCFT, VN-EAEU; special preferential import tax rates may be higher than preferential rates.

– Common import tax: This is a standard tariff rate for goods originating from countries with which Vietnam does not participate in preferential trade agreements or does not have MFN treatment. The common import tax rate is generally 150% of the preferential tax rate for each corresponding item. In cases where the preferential tax rate is 0%, the Prime Minister decides on the application of the common tax rate based on Article 10 of this Law.

– Additional tax: In addition to import duties, certain goods may also be subject to additional taxes in the following cases:

- The selling price of imported goods is significantly lower than the domestic price, causing difficulties for the production of similar goods in our country.

- Goods imported from countries or territories that differentiate treatment of imported goods or import duties on Vietnamese goods.

Time of Import Tax Calculation

According to the Law on Export and Import Duties 2016, the time of import tax calculation is when registering the customs declaration before the goods arrive at the border gate or within 30 days from the date the goods arrive at the border gate.

Current Types of Import Taxes

Classification by Calculation Method

In cases where import duties are classified by calculation method, there are two types of customs duties:

– Ad valorem tariff: A percentage rate on the CIF price of imported goods.

– Specific tariff: Calculated based on the weight of imported goods (e.g., $5 per ton).

Classification by Taxation Purpose

In cases where import duties are classified by taxation purpose, there are three types of customs duties:

– Revenue-generating import tax: A tax primarily aimed at increasing state budget revenue rather than protecting domestic production.

– Protective import tax: A tax intended to artificially increase prices of imported goods to protect domestic production from foreign competition.

– Prohibited import tax: A high-rate tariff almost no importer dares to import such goods anymore.

Detailed Calculation Methods for Import Tax

Corresponding to each method of import tax calculation, there are specific calculation formulas:

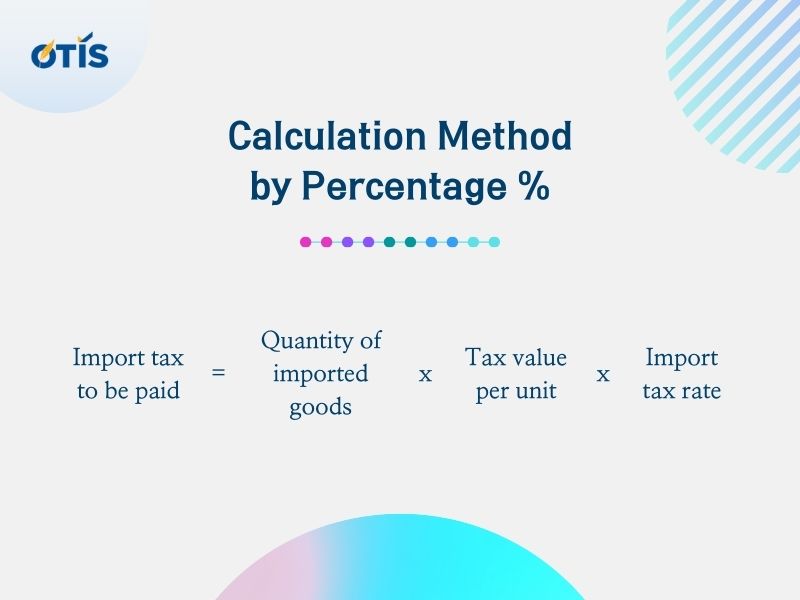

Calculation Method by Percentage %

For the calculation method based on percentage %, the import tax amount to be paid is determined based on the value of imported goods and the percentage tax rate of each item at the time of taxation.

Specifically, the formula for calculating import tax by percentage % is as follows:

Where:

Tax value per unit: The customs value specified in the Customs Law.

Import tax rate: Specifically stipulated for each item in the export tax schedule.

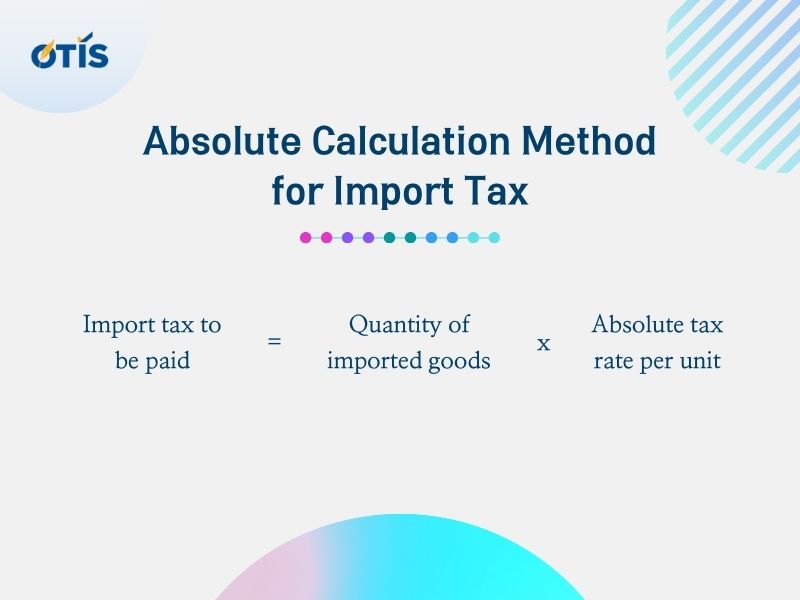

Absolute Calculation Method for Import Tax

For the absolute calculation method, the import tax amount to be paid is determined based on the quantity of imported goods and the absolute tax rate per unit of goods at the time of taxation.

Specifically, the formula for calculating absolute import tax is as follows:

Note: To determine the tax rate for each item, businesses need to consider:

– Nature and structure of imported goods.

– Application of 6 classification rules in Appendix II issued with Circular No. 103/2015/TT-BTC.

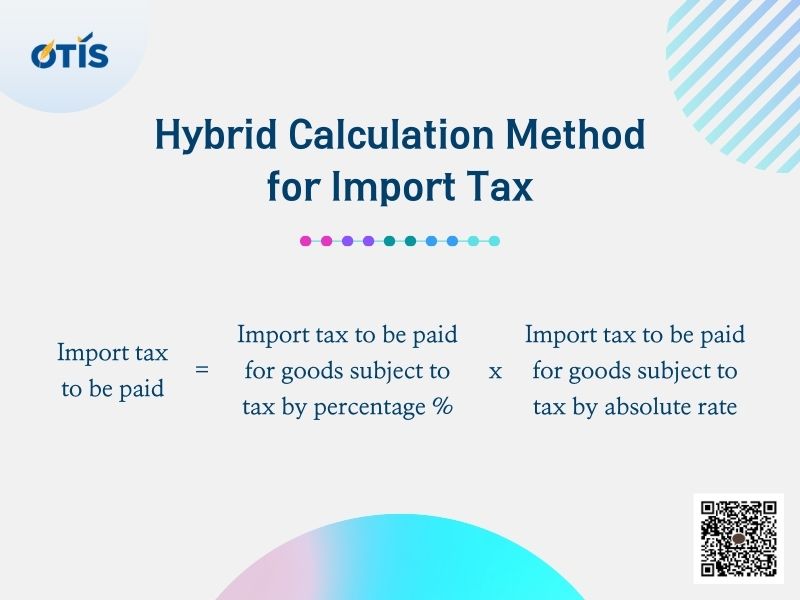

Hybrid Calculation Method for Import Tax

For the hybrid calculation method, the import tax amount to be paid is determined based on the total tax amount based on the percentage % and the total tax amount based on the absolute rate.

Specifically, the formula for calculating hybrid import tax is as follows:

For any questions or comments, please contact:

OTIS AND PARTNERS LAW FIRM

Office address: 2nd Floor, CT3 Building, Yen Hoa Park View Urban Area, No. 3 Vu Pham Ham Street, Yen Hoa Ward, Cau Giay District, Hanoi

Email: info@otislawyers.vn

Hotline: 0987748111

{kind=link}

{kind=link}