Tiếng Việt

Tiếng Việt 한국어

한국어 中文 (中国)

中文 (中国)Currently, some opinions suggest that Vietnam lacks specific regulations regarding mergers and acquisitions (M&A) activities, which leads to the unofficial recognition and underdevelopment of M&A activities. However, not every country worldwide has comprehensive legislation governing M&A activities. According to a study by the Enterprise Law and Investment Law Enforcement Team, countries like the United States, Canada, Japan, and China do not have separate laws specifically for M&A activities. Instead, M&A activities are regulated by various intertwined legal provisions such as Competition Law, Anti-Monopoly Law, and Company Law. The M&A market in Vietnam existed before the Competition Law, the first legal document addressing this issue, was enacted. To conduct M&A transactions, investors must adhere to many specific legal regulations governing various aspects of this activity, such as Competition Law, Enterprise Law, Investment Law, Securities Law, and Labor Law.

Rights in M&A

From the perspective of enterprises, Vietnamese laws recognize the rights of investors to carry out M&A transactions, as stipulated in the Investment Law, Enterprise Law, Securities Law, Civil Law, and Credit Institutions Law. These rights include the right to purchase shares, the value of capital contributions of capital owners, the value of the company’s shares, the right to sell the enterprise (including selling the assets of the enterprise, transferring all owned capital contributions, or selling the entire state-owned enterprise), and the right to repurchase enterprises from Vietnamese economic organizations.

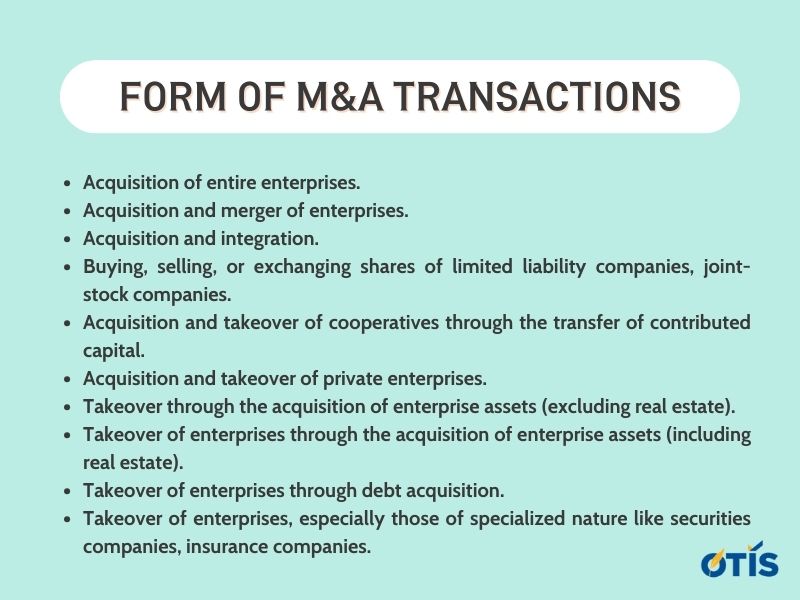

With the recognition of these rights, various forms of M&A transactions have been implemented in practice, such as:

- Acquisition of entire enterprises.

- Acquisition and merger of enterprises.

- Acquisition and integration.

- Buying, selling, or exchanging shares of limited liability companies, joint-stock companies.

- Acquisition and takeover of cooperatives through the transfer of contributed capital.

- Acquisition and takeover of private enterprises.

- Takeover through the acquisition of enterprise assets (excluding real estate).

- Takeover of enterprises through the acquisition of enterprise assets (including real estate).

- Takeover of enterprises through debt acquisition.

- Takeover of enterprises, especially those of specialized nature like securities companies, insurance companies.

Legal Procedures Related to M&A Forms

The M&A forms mentioned above are based on corresponding legal procedures for registration with competent state agencies, ranging from the registration procedures for merging and consolidating 100% Vietnamese-owned companies, companies with foreign direct investment (including companies of the same or different types or private enterprises) to purchasing state-owned enterprises.

However, in some industries, Vietnamese laws or Vietnam’s international commitments do not clearly define the rights of foreign investors to participate in the market, leading to some competent state agencies refusing to license foreign investors to contribute capital or purchase shares in Vietnamese enterprises. The concept of “foreign investors investing in Vietnam for the first time” also has different interpretations, resulting in inconsistent legal application among localities. This reality has been and continues to be a barrier to foreign investment inflows through M&A activities.

Additionally, M&A activities are hindered by the mechanism and procedures for opening investment capital accounts. The State Bank has issued several documents regarding this matter, but most of these documents are conflicting and unclear, such as regulations on the compulsory application of “investment capital accounts” for share transfer forms of shareholders, investors outside Vietnam’s territory, and capital transfer within enterprises with foreign investment. Moreover, the requirement to open “investment capital accounts” will limit the method of repurchasing through “debt deduction” by restructuring the enterprise.

For merger cases, where the merging company and the receiving company hold a market share from 30% to 50% in the relevant market, the company must notify the competition management authority before proceeding with the merger, unless competition laws stipulate otherwise. Merger, consolidation is prohibited when the merged company, the receiving company holds a market share of over 50% in the relevant market. However, how can enterprises determine their market share in the relevant market to proactively notify the competition management authority if they fall under the cases specified by the law? This determination mechanism has not been legalized for enterprises and state management agencies to implement.

The Enterprise Law and Decree 43/2010/ND-CP on enterprise registration do not specify that the merger dossier must include a notification from the enterprise to the competition management authority. Therefore, the enterprise registration authority cannot determine whether the merger violates competition management regulations. Additionally, the law does not regulate the coordination mechanism between the competition management authority and the enterprise registration authority in managing enterprise merger activities. Thus, this issue needs to be addressed in the future.

Accounting and Tax Mechanisms

Current regulations regarding accounting and tax regimes for M&A cases are relatively specific through laws on accounting, tax administration, value-added tax, and corporate income tax. A study on “Legal Regulation of Mergers and Acquisitions in Vietnam” conducted by independent experts from the Enterprise Law and Investment Law Enforcement Team identified that companies do not encounter legal difficulties related to accounting and tax issues when engaging in division, separation, merger, and consolidation of enterprises.

Conversion of shares, bonds, securities, and enterprise assets in the merger and consolidation process

The purchase of enterprises through assets other than cash is recognized by current legal regulations. These other assets may include freely convertible foreign currency, gold, land use rights value, intellectual property ownership rights, technology, technical know-how, shares, stocks, debts, trademarks, industrial designs, and other assets specified in the company’s charter.

However, the State Bank of Vietnam recently issued a regulation stipulating that the currency used to contribute capital or purchase shares in Vietnamese enterprises is the Vietnamese dong. The currency used for payment when purchasing enterprises owned 100% by the state is also the Vietnamese dong. Vietnamese investors are allowed to transact in foreign currencies in investment activities and use foreign currencies for overseas investments. This regulation has created inconsistencies in the forms of capital contribution, share purchase, and acquisition of Vietnamese enterprises, posing difficulties for investors, especially foreign investors.

Labor

The Labor Code specifies that in cases of merger, consolidation, division, separation of enterprises, transfer of ownership rights, management rights, or use rights of enterprise assets, the succeeding employer must continue to fulfill the labor contract signed with the employee. In cases where employment is not fully utilized, leading to termination of employment contracts, employees must receive job loss allowances equivalent to one month’s salary for each year of service, but not less than two months’ salary. This is an issue that acquiring enterprises must carefully consider complying with legal requirements and align with the investment costs of the enterprise.

Another drawback is that if the labor utilization plan proposed by the acquiring enterprise is objected to by the grassroots trade union or the provincial labor authority, it can be renegotiated with the trade union, but it is unclear how to negotiate with the provincial labor authority. If the collective of employees opposes the labor utilization plan or does not agree with the trade union’s viewpoint on the labor utilization plan, it will also affect the merger and consolidation process of the enterprise.

Competition and Economic Concentration

As mentioned above, the purchase, sale, and acquisition of enterprises are forms of economic concentration within the scope of regulation of the Competition Law. There are cases where the acquisition of enterprises is not considered economic concentration, such as “the case of insurance companies, credit institutions acquiring other enterprises to resell within the longest period of one year.”

The competition law also provides for prohibited economic concentrations, such as when the combined market share of participating enterprises in economic concentration exceeds 50% in the relevant market, except in cases where “one or more parties to the economic concentration are at risk of dissolution or bankruptcy”; or “have the effect of expanding exports or contributing to the development of the economy – society, technological progress”, or “after the economic concentration, they still belong to the category of small and medium-sized enterprises as prescribed by law.”

Overall, Vietnamese law currently acknowledges the right to merge, consolidate, acquire enterprises, and cooperatives of both domestic and foreign investors.

M&A activities will bring significant investment sources to Vietnam and enhance the country’s ability to absorb management and production technologies. In the context of financial crises and business restructuring, M&A activities can further expand opportunities for Vietnamese enterprises to access global markets and create a solid global presence for Vietnamese enterprises.

For any questions or comments, please contact:

OTIS AND PARTNERS LAW FIRM

Office address: 2nd Floor, CT3 Building, Yen Hoa Park View Urban Area, No. 3 Vu Pham Ham Street, Yen Hoa Ward, Cau Giay District, Hanoi

Email: info@otislawyers.vn

Hotline: 0987748111

{kind=link}

{kind=link}